One of the biggest mountains to climb is scaling your small business as it starts to grow. Cash flow can be an issue, along with the simple logistics of getting supplies from manufacturer to customer. Going from a mom-and-pop size operation to something more significant requires juggling many moving parts.

Your business will grow rapidly if you have a passion for what you do. If you’re new to operating a company, you may feel uncertain what your next steps should be.

What Makes Some Businesses Thrive?

According to the U.S. Bureau of Labor Statistics, many companies easily make it through their first year. Although the numbers vary, data from the past 18 years shows that 75.2% to 96.2% of small businesses survive the first 12 months.

The early days are filled with excitement and passion. It is when a business starts to grow that many people feel overwhelmed. They may struggle to keep cash flowing to cover supplies while ramping up order fulfillment.

Some challenges include staffing, marketing, bookkeeping, sourcing and logistics. Fortunately, you can learn what you need to know to scale your business and become one of the millions of small-business success stories.

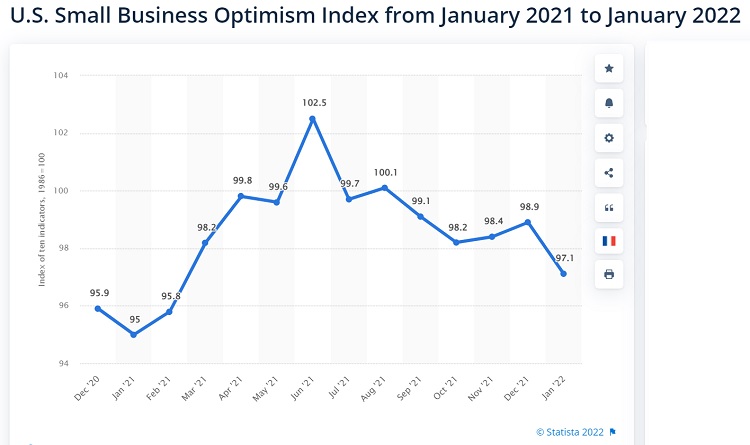

Many businesses are also facing additional challenges due to the Optimism Index, which has been fluctuating during the pandemic.

Source: https://www.statista.com/statistics/220353/monthly-us-small-business-optimism-index

A truly scalable business doesn’t rely on business or consumer fluctuations but plans for all situations.

1. Check Your Timing

Make sure the timing is right before you scale your business. Figure out whether you have the systems and finances in place to support growth.

For example, if you get a contract with a big box store, they may want you to send inventory and not pay you until it sells through or at least on a 60-days net contract. You’ll need enough funds to order and send products without getting paid right away.

You also need to know how to handle increased volume should your business suddenly take off. Most experts recommend defining specialized roles and strengthening management to handle the additional workload.

2. Invest in Technology

Scaling up means you either have to work harder or smarter. Fortunately, today’s technology allows you to automate many processes. Your warehouse is an obvious first place to start with automation. You could install machines that pick orders so all an employee has to do is ensure everything is present and seal the box.

Ensuring you have systems in place before you expand means you can meet demand even if you’re short on employees or haven’t yet hired enough people to cover the increased workload.

3. Enhance Skills

Growing means you need more skills and knowledge on your team. Spend time training your current workers in methods they’ll need to know as the brand grows, and focus on efforts to retain them. You should also seek new employees who can fulfill roles a larger company requires.

Pay careful attention to management and the unique knowledge each person brings. Do you have enough department heads to oversee big projects and orders? As you prepare for growth, look at your systems, organizational structure and leadership every three months or so. Meet, evaluate and make adjustments as needed.

Your department heads are your best source for what you need for successful scalability.

4. Know Your Target Audience

You need to know your current customers and how they fit into your growth plans as you expand. For example, if you’ve sold directly to consumers but now want to enlist the help of a big-box retailer to move your product, what happens to your current customer base?

How can you handle wholesale and retail operations and do justice to business-to-business (B2B) and business-to-consumer (B2C) customers?

Improve your user experience now so they are happy with your brand when you gain new customers. One of the most successful strategies businesses adopt is creating a positive UX on their websites. The effort improves SEO and customer satisfaction.

Source: https://www.marketingcharts.com/digital/seo-79942

When asked what improves SEO most, around 34% of SEO specialists cited UX. Think about your audience and what helps them most.

5. Increase Your Revenue

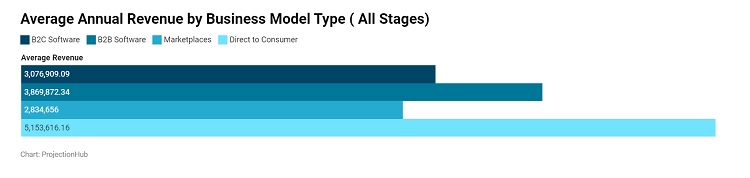

There are two ways you can increase your bottom line. You can either gain more customers or make more money on the items you sell. ProjectionHub conducted a Startup Revenue Study recently. It analyzed 234 startups across different business models and found the average revenue was around $3 million for B2C tech companies.

Source: https://www.projectionhub.com/post/startup-revenue-stats-a-study-of-234-tech-startups-2022

Obviously, not all that money was profit. The average entrepreneur may make around $50,000 with a solopreneur operation. There are varying levels in small and medium businesses for how much revenue you bring in.

No matter where you currently are, deciding if you want to take on more customers, increase the amount for each sale or both can make a difference in how you scale.

6. Define a Sales Strategy

Get everyone on your sales team on the same page by laying out your policies and what you’re going for. Is your goal to ramp up packages and increase revenue from current customers? Then the push would be to touch base with clients and explain new products and how you can help them in their life or business.

On the other hand, reaching new customers means getting out to business events, making cold calls, ramping up marketing, and answering questions about your company and products.

7. Learn to Delegate

Many entrepreneurs get used to wearing different hats. They learn quickly that others don’t always do things up to their standards, so they tend to just do it themselves. The problem with an independent mindset is that you spend a lot of time on tasks others can do adequately.

Figure out what is vital for you to do and learn to farm out other jobs. Let go of your control and hire the best people possible so you can trust them to complete the work at least close to the way you would.

Your management team must become responsible for the staff’s work quality under their direct supervision. Train your team to be mini CEOs and give them a reason to want to help the company grow.

8. Watch Cash Flow

One issue failed business owners cite again and again for going under is lack of cash flow. In fact, around 82% of businesses cite money issues as the reason they fail.

You must have enough money to endure the ups and downs of rapid growth before you try to scale. An emergency fund is necessary, but you also have to free up money to cover unexpected expenses and delayed payments.

Know where you’ll get money if you need it in a pinch, such as through investors, family and friends, or a loan. Go into your growth phase with a solid plan in place.

Plan for the Worst, Expect the Best

When it comes to scaling your business, you should always prepare for the worst. Ideally, good things will happen, your company will thrive and you’ll have some extra cushion in your budget.

Just as you wouldn’t buy a building and not have insurance on it in case of a tornado or flood, you also must expect the unexpected for day-to-day operations and prepare accordingly. A scalable business can pivot in a millisecond and keep moving forward. Hire the right people, save enough money and prepare for all contingencies, and you’ll do well.

Eleanor Hecks is editor-in-chief at Designerly Magazine. She was the creative director at a digital marketing agency before becoming a full-time freelance designer. Eleanor lives in Philadelphia with her husband and pup, Bear.